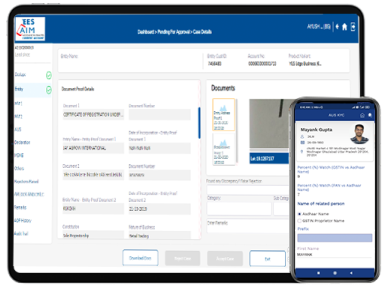

Effortlessly streamline your digital onboarding solutions with our intuitive no-code platform, Vahana Cloud. It not only covers a full range of liability portfolios but also enables both self-onboarding and assisted journeys.

Empower your customers with a seamless and user-friendly operation platform that is designed for a variety of onboarding scenarios. Additionally, customize onboarding experiences to meet specific customer needs, manage user data effortlessly, and provide top-notch support to foster lasting relationships.

Sales Platform

Boost your sales team's efficiency with automated pipelines and real-time analytics. Effortlessly track leads, optimize sales funnels, and close deals faster using our comprehensive no-code sales solutions

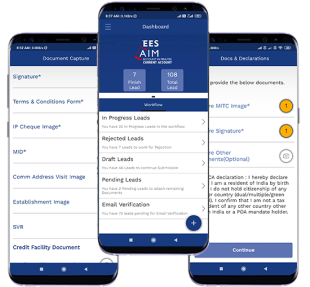

Operation Platform

Moreover, simplify your operations with automated workflows and integrated management tools. As a result, you can monitor processes, ensure compliance, and streamline tasks to keep your operations running smoothly and efficiently.

Expand your Capabilities with these Additional Tools

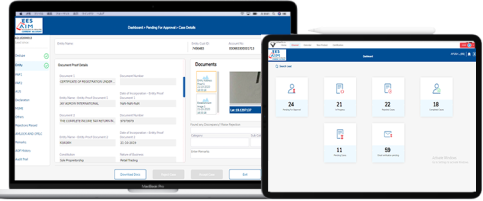

Asset Management

Effortlessly manage your bank's asset portfolios with our innovative no-code solutions. Furthermore, automate asset tracking, optimize resource utilization, and gain actionable insights to maximize the value and performance of your financial assets.

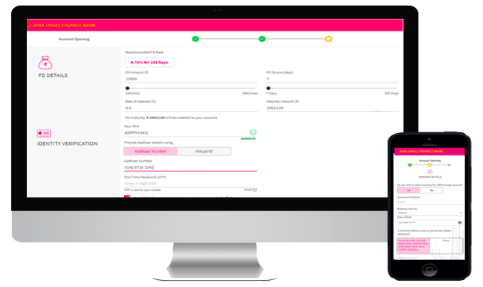

Liability

Management

In addition, streamline your bank's liability management with our powerful platform. Automate liability tracking, ensure full regulatory compliance, and effectively mitigate risks to maintain control over your bank's liabilities.

Yasas Kalki is the President of Sales – India. Having 25+ years of industry experience, he spent 12 years at Salesforce, achieving outstanding sales performance and building strong client relationships in the Enterprise business. He has also worked at Accenture, Infosys, GE Capital, Innoveer Solutions, and Sonata Software.