As Warren Buffett once said, “Risk comes from not knowing what you’re doing.” In today’s underwriting landscape, that wisdom takes on new meaning. We’re not just managing the risks we underwrite; we’re navigating the risks and opportunities of AI itself.

The AI Underwriting Revolution Is Real (And It’s Already Here)

Here’s something that will catch you off guard. The AI underwriting market has exploded from $2.85 billion in 2024 to a projected $11.92 billion in 2029. That’s growing at 33% every single year, which tells us this isn’t some far-off future thing we can think about later. It’s happening right now, whether we’re ready or not.

And look, we get the skepticism. We’ve all been through enough “revolutionary technology” cycles to have our guard up. Companies implementing AI underwriting systems have slashed processing times by up to 90%, turning what used to take weeks into mere hours. Things that used to take us weeks are now wrapping up in hours.

Life insurance applications that involved weeks of chasing down medical records? Some carriers are turning those around in minutes for straightforward cases.

But here’s the part that doesn’t make it into most headlines. The companies seeing real success aren’t just throwing AI at everything and hoping for the best. They’re keeping humans involved in ways that actually matter.

What AI Underwriting Does Brilliantly

Before we talk about where humans matter most, let’s give credit where it’s due. AI underwriting excels at several critical functions that used to consume enormous amounts of underwriter time and attention.

Think about data ingestion and risk digitization. AI platforms can pull information from dozens of disparate sources, from credit scores and medical records to IoT devices and social media patterns, then standardize and synthesize it into a coherent risk profile. What once took underwriters hours of manual data entry and cross-referencing now happens in seconds. One major insurer reported reducing pre-quote data preparation by 40% using cognitive AI, freeing their underwriters to focus on what actually requires expertise.

The pattern recognition capabilities of machine learning are equally impressive. AI can analyze historical claims data across millions of policies, identifying risk factors and correlations that would be impossible for any human to spot manually. These predictive analytics models can forecast future claims with increasing accuracy, helping insurers set premiums more precisely and identify fraud patterns that might otherwise slip through.

For routine, straightforward submissions, AI underwriting delivers remarkable consistency and speed. A standard auto or home policy with no unusual risk factors? AI can assess it, price it, and issue it faster and more consistently than any human underwriter working alone. This isn’t just about efficiency; it’s about freeing up your most skilled professionals to work on what actually needs their expertise.

Where Human Judgment Becomes Non-Negotiable

Now here’s where it gets interesting. Despite all the impressive capabilities of AI underwriting, there are critical areas where human judgment isn’t just valuable—it’s absolutely necessary.

The Nuance Problem

Consider a commercial insurance submission for an emerging technology company. The business model is innovative, the industry is nascent, and the historical data is limited. AI can process whatever data exists, but it can’t contextualize what isn’t in the dataset yet. It can’t understand the broader market dynamics, anticipate how regulatory frameworks might evolve, or assess the quality of the management team based on subtle cues in their responses to questions.

As one underwriting executive put it during a recent industry symposium, “Trust is critical to our business. The type of insurance we write is very sophisticated and directly impacts the executive team and the board of directors. That pool of individuals doesn’t want to trust an online solution. They want to work with expert brokers and underwriters who have demonstrated a deep understanding of their business.”

Human underwriters bring contextual understanding that goes beyond data points. They can read between the lines, pick up on inconsistencies that aren’t obvious in the numbers, and apply professional judgment based on years of experience seeing how similar situations played out.

The Ethics and Fairness Imperative

AI is only as unbiased as the data it learns from. And let’s be honest about our historical data, it’s got bias baked into it. Machine learning models can accidentally amplify those biases instead of fixing them.

The regulators are catching on. New York’s Circular No. 1 is pretty explicit about this. Insurers need governance frameworks; they need to explain how AI influences decisions, and they need humans watching to make sure the algorithms aren’t perpetuating unfair practices.

An algorithm can assist with risk assessment, but it cannot be held accountable. Only a human underwriter can take responsibility for ensuring that pricing decisions are fair, that coverage isn’t being unfairly denied to certain groups, and that the application of underwriting guidelines aligns with both regulatory requirements and ethical standards.

Complex Risk Assessment

Not every risk fits neatly into a data model. When you’re underwriting a niche industrial operation, a first-of-its-kind event, or a business with unique circumstances, you need an underwriter who can think critically beyond the available datasets.

Human underwriters excel at assessing non-standard risks. They can evaluate factors that might not be captured in structured data—the quality of a company’s safety culture, the credibility of management’s risk mitigation plans, or the unique exposures of an emerging industry segment. These are judgment calls that require discretion, industry knowledge, and the ability to make reasoned decisions in ambiguous situations.

The Client Relationship

Insurance isn’t just a transaction; it’s a relationship built on trust. Brokers and insureds want explanations, negotiations, and the confidence that comes from working with someone who truly understands their situation.

AI can summarize a submission, but it can’t discuss a complicated coverage structure with a broker, walk them through why an exception might or might not be possible, or build the credibility that comes from years of demonstrated expertise. These relationship elements matter enormously, especially in commercial lines and specialty insurance where accounts are complex and long-term partnerships are the norm.

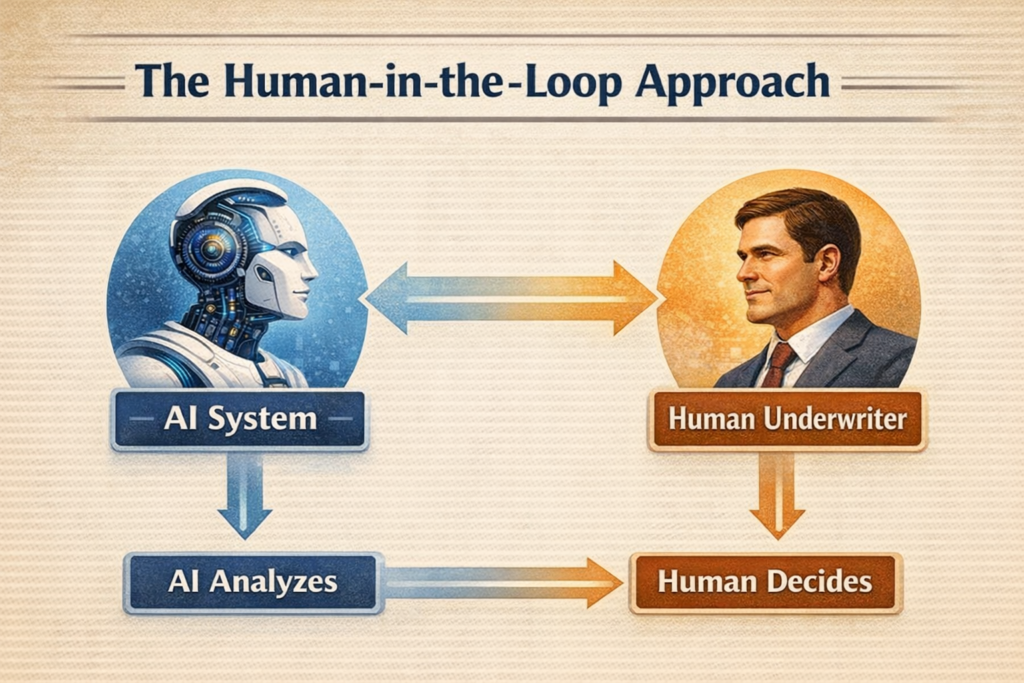

The Human-in-the-Loop Model: Best of Both Worlds

The most successful insurance organizations aren’t choosing between AI and human underwriters—they’re building workflows that combine the strengths of both. This “human-in-the-loop” approach is emerging as the industry standard for good reason.

Here’s how it typically works in practice. AI processes incoming submissions, extracting key data points and conducting initial risk assessments. For straightforward cases that fall clearly within appetite and guidelines, the AI can move toward automated approval, with a human underwriter reviewing and confirming the decision. For cases where the AI identifies low confidence in its assessment, or where the risk characteristics are unusual, the system routes the submission to a human expert for detailed review.

The human underwriter provides corrections and adjustments based on their expertise, and critically, these corrections feed back into the AI system to improve its future performance. Over time, the AI gets better at recognizing patterns, but the human remains in control of the strategic decisions, the complex assessments, and the relationship management.

This approach delivers dramatic productivity gains—some insurers report their underwriters can process five times more submissions while maintaining control and accuracy—while preserving the judgment, accountability, and relationship value that humans provide.

What This Means for the Future of Underwriting

Albert Einstein reportedly said, “The true sign of intelligence is not knowledge but imagination.” In underwriting, we might adapt that to say the true sign of effective risk assessment is not just data processing but judgment.

The role of underwriters is evolving, not disappearing. Routine work is being automated, allowing professionals to focus on higher-value activities. The underwriters who will thrive in this new landscape are those who embrace AI as a powerful tool that amplifies their expertise rather than viewing it as a threat.

Think of it like this: calculators didn’t eliminate the need for mathematicians; they freed them from tedious arithmetic to focus on complex problem-solving. Similarly, AI underwriting doesn’t eliminate the need for skilled underwriters—it frees them from data entry and routine cases to focus on the work that genuinely requires expertise, judgment, and human insight.

Practical Considerations for Implementation

If you’re considering implementing AI underwriting in your organization, here are some key principles to keep in mind based on what successful adopters have learned.

Start with high-impact, well-defined use cases. Document processing, data extraction, and submission intake are excellent starting points because they deliver immediate ROI while being relatively straightforward to implement. Don’t try to automate everything at once—build confidence and capability incrementally.

Invest heavily in data quality before implementing AI. Several insurers have reported that spending months organizing and standardizing their historical data before deployment paid enormous dividends in system accuracy and performance. AI is only as good as the data it learns from.

Keep your underwriters involved throughout the implementation process. They’re not just the end users—they’re the subject matter experts who can identify where AI will add the most value and where human judgment needs to remain central. Organizations that treat AI implementation as a collaborative effort between technology teams and underwriting teams see better outcomes than those who hand down solutions from on high.

Build strong governance frameworks from the beginning. Clear protocols for when AI handles decisions autonomously, when it makes recommendations for human review, and when cases must go straight to expert underwriters are essential. Regular audits to check for bias, accuracy, and alignment with underwriting guidelines should be built into your process, not added as an afterthought.

The Competitive Landscape Is Moving Fast

Here’s the reality: while thoughtful implementation matters, speed matters too. The window for competitive advantage through AI adoption is rapidly closing. Organizations that hesitate while competitors deploy intelligent automation risk finding themselves permanently disadvantaged in an increasingly data-driven marketplace.

According to recent industry surveys, AI and generative AI adoption in underwriting is expected to jump from just 14% today to 70% in the next three years. That’s not a gradual shift—it’s a wholesale transformation of how underwriting operates.

The insurers who succeed won’t be those who automate the most or those who resist automation entirely. There will be those who draw the line thoughtfully, building strong human-in-the-loop workflows that enhance underwriter judgment rather than trying to replace it.

Also Read: AI and No-Code: A Catalyst for Inclusive Financial Services

Looking Ahead: Underwriting in 2030

What might underwriting look like five years from now? The technology will certainly be more sophisticated. We’re already seeing early examples of AI agents that can handle entire customer onboarding workflows, coordinating with other AI agents to build risk profiles, suggest policy structures, and ensure regulatory compliance.

But even in this more automated future, the fundamental need for human judgment won’t disappear—it will become more concentrated and more valuable. The strategic oversight of portfolio risk, the assessment of truly novel exposures, the relationship management with key brokers and clients, and the ethical oversight of AI-driven decisions will remain firmly in human hands.

The winners will be organizations that use AI to eliminate the drudgery of underwriting while preserving and enhancing the expertise, judgment, and relationship value that skilled underwriters provide.

As we navigate this transformation, perhaps we should remember the words of Henry Ford: “Coming together is a beginning, staying together is progress, and working together is success.” The future of underwriting isn’t human or AI—it’s human plus AI, working together to achieve what neither could accomplish alone.

The underwriters who embrace this partnership, the organizations that implement it thoughtfully, and the leaders who invest in the right balance of automation and expertise will define the next era of insurance. The question isn’t whether to adopt AI underwriting—it’s how to do it in a way that preserves the judgment, ethics, and human insight that will always matter in risk assessment.

People Also Ask

What is AI underwriting in insurance?

AI underwriting uses artificial intelligence and machine learning to automate and enhance the insurance risk assessment process. It analyzes vast amounts of data from multiple sources, identifies patterns, and makes pricing recommendations. While AI excels at processing routine submissions quickly, human underwriters remain essential for complex cases, ethical oversight, and relationship management with clients and brokers.

How does AI improve the underwriting process?

AI dramatically reduces processing times by up to 90%, turning weeks of work into hours. It excels at data extraction, pattern recognition across millions of policies, and fraud detection. AI also ensures consistency in routine decisions and frees underwriters from manual data entry, allowing them to focus on complex risks that require professional judgment and expertise.

Can AI replace human underwriters?

No, AI cannot fully replace human underwriters. While AI handles routine cases efficiently, humans remain essential for nuanced risk assessment, ethical oversight, complex commercial risks, and client relationships. The most successful approach combines both through human-in-the-loop workflows, where AI handles data processing while humans make final decisions on complex or unusual submissions.

What are the risks of using AI in underwriting?

The primary risks include perpetuating bias from historical data, lack of transparency in AI decision-making, and regulatory compliance challenges. AI may struggle with novel risks lacking historical data and cannot be held accountable for decisions. This is why regulators require human oversight, clear governance frameworks, and documentation to ensure fairness and prevent discriminatory practices in underwriting.

What is human-in-the-loop AI underwriting?

Human-in-the-loop AI underwriting combines automated processing with human expertise. AI handles initial data extraction and assessment, automatically processing straightforward cases while routing complex or unusual submissions to human underwriters. Underwriters review AI recommendations, make corrections, and provide final approval. Their feedback continuously improves the AI system while maintaining accountability and preserving critical human judgment.