India has a brand new payment option called the eRupi. What is the eRupi? What can it do? How does it help? eRupi is essentially a digital voucher. Remember Sodexo coupons for employee benefits? Well, think of eRupi as a digital version of the same with much more exhaustive and nuanced use-cases.

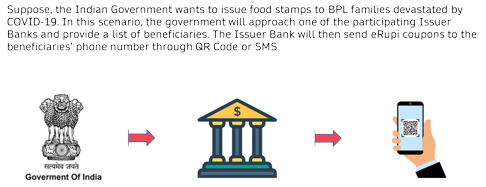

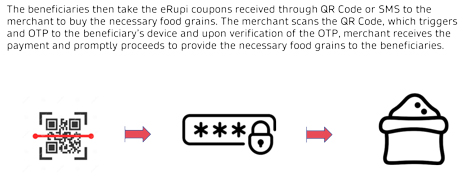

Developed by the National Payments Corporation of India (NPCI) on its UPI platform, in collaboration with the Department of Financial Services, the Ministry of Health and Family Welfare, National Health Authority, and 11 partner banks, the e-RUPI voucher will be delivered in the form of a QR code or SMS string-based e-voucher to the beneficiary’s mobile number. It would enable person-specific, purpose-specific digital contactless payment. Banks, PSPs, and entities which hold licenses for prepaid instruments can issue these vouchers, and a maximum payment of INR 10,000 can be made via them. But these are single transaction and non-transferable vouchers. eRupi does not permit direct cash withdrawal or peer-to-peer transfer. A government agency can approach a bank to issue vouchers to an identified set of beneficiaries who are then sent a QR Code or SMS-based voucher on their mobile phone. The beneficiary can take this to a merchant and, using an OTP, redeem it at the merchant location to purchase the product/service for which the voucher was issued. The merchant only needs an app to scan the code and accept the voucher

These vouchers can be used for a multitude of use-cases such as healthcare to enable vaccination payments, subsidy transfers, and food entitlements, etc. And since the beneficiary does not need to download a separate application to access vouchers, availing services through eRupi will be very easy for beneficiaries who are not digitally savvy and thereby help such beneficiaries to become a part of the digital economy. eRupi could also go a long way in plugging leakages in PDS. The JAM trinity (Jan Dhan Account, Aadhaar, and Mobile) has successfully been able to cut down leakages, but a lot of o beneficiaries have been struggling due to Aadhaar biometric rejections. eRupi also ensures that funds disbursed for a specific purpose are used for that purpose and that purpose only since they cant be encashed or transferred.

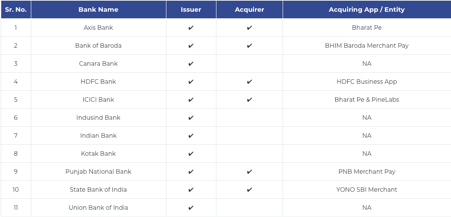

Banks Live with e-RUPI –

As is the case with all digital payments methods, there are some security risks to ponder about such as sharing or stealing vouchers. To prevent this, there must be a two-step verification process to identify the services being delivered and that they are delivered to the correct beneficiary. QR-based payments may give rise to Qshing or QR code abuse and allow hackers to use social engineering to gain access to the beneficiary’s personal data in a single scan. Hence, eRupi needs a resilient cybersecurity framework backing the payment instrument and grievance redressal mechanisms must be put in place to address the lags and user concerns.